Are Money Market Funds a Good Investment?

Exploring the Benefits and Risks of Money Market Funds

In recent years, the landscape for money market funds (MMFs) has shifted dramatically. After a prolonged period of minimal returns tied to the Federal Reserve’s near-zero interest rate policy, MMFs began offering yields above 5%. This change has made MMFs an attractive option for investors looking for higher returns on their cash holdings.

Why Money Market Funds are Attractive

At the same time, longer-term bond yields also increased but stayed below MMFs, creating a compelling case for holding cash over traditional bond investments. Consequently, the yield differential enticed investors to keep more cash in these funds. Since the Fed started hiking rates in 2022, assets in MMFs grew by 26% to $6.4 trillion (Figure 1). Looking forward, this anomaly of higher yields on MMFs than longer-term bonds may not continue, and investors should approach holding large amounts in MMFs with caution.

Figure 1:

Source: St. Louis Federal Reserve Bank, as of July 31, 2024.

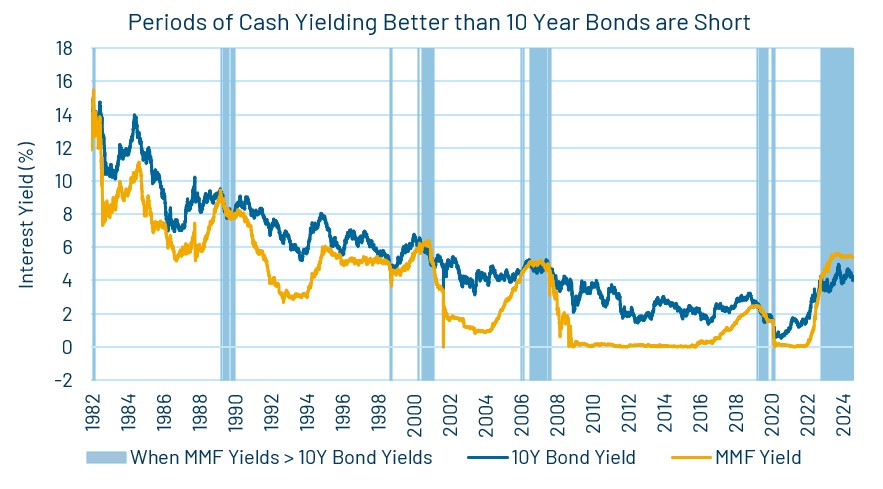

Historical Context and Future Predictions

Historically, such favorable conditions for MMFs are rare. Periods of MMFs yielding more than intermediate-term bonds are typically short, happening only 9.4% of days since 1982, with most of those days occurring in the past two years. Prior to October 2022, higher MMF yields only occurred 5.7% of days. Thus, today’s trends may not hold tomorrow, and investors cannot assume this will continue.

Figure 2:

Source: St. Louis Federal Reserve Bank, as of July 31, 2024.

Upcoming Changes in Interest Rates

Currently, all indicators point towards the Federal Reserve beginning a rate-cutting cycle as early as September. Futures markets predict a 1.5% reduction in rates over the next year. Given this, the current 5% yield offered by MMFs is unlikely to persist since MMF yields move with short-term rates.

The correlation between Fed funds rates and short-term Treasury yields is well-documented. As the Fed reduces overnight rates, yields on short-term bonds, including those held in MMFs, are expected to decrease as well. This presents a dilemma for investors with significant holdings in MMFs: balancing the need for liquidity with the imperative to secure competitive returns.

Comparing Money Market Funds and Bonds

Importantly, simply comparing yields on MMFs to bonds cannot tell you which asset will perform better. Last year, despite higher MMF yields, 84% of all bond mutual funds and ETFs outperformed the taxable money market average return of 4.7%. Additionally, when considering longer-term bond options, despite their lower current yields of 3.9% for 5-year and 4.1% for 10-year bonds, these bonds may offer a more stable investment. These yields are locked in, providing a hedge against the potential decline in MMF yields.

Making Informed Investment Decisions

Investors navigating these complexities should seek advice that aligns with their financial goals. Holding cash in an MMF for short-term spending needs can make sense for investors, but this decision should be made in conjunction with overall financial planning. Working closely with financial advisors ensures that investment decisions are grounded in comprehensive analysis and tailored strategies. By maintaining a focus on goals-based asset allocation, investors can better manage the challenges posed by the evolving MMF landscape and interest rate environment.

[1] As of 7/31/24

[2] Blackrock, as 2/29/24

[3] As of 7/31/24